Capital Allocation Snapshot: Berkshire Hathaway

Over the past month I have been trying to build momentum with my Substack by writing about Berkshire Hathaway as a lead up to the annual meeting (that I went to). Now that the meeting is over, I am capping off this theme by taking a look at how Warren Buffett has allocated capital at Berkshire for the last five years. Most companies do a poor job of reinvesting profits, either by investing it into low growth projects, make dumb acquisitions, or buyback overpriced stock. Buffett is the master of capital allocation, and his writings over the years have highlighted the importance of intelligent capital allocation. With that, let’s jump in to get a quick overview of how Berkshire has recently reinvested their cash.

Cash Flow Summary

The first place to start when summarizing Berkshire’s cash flow statement is to look at cash from operations. BRKs cash from operations has been very stable the past 5 years, hovering around $37B. I am a little surprised this figure has not been growing, but maybe there is a reasonable explanation.

Over the past 5 years, Berkshire has been generally spending money on investments. The exception is 2021, where they realized $29B in gains, which is comparable to their cash from operations. As expected, the purchase and sale of equities is important to the cash from investing, but Berkshire buys and sells a lot of fixed income securities as well.

BRKs cash from financing has been relatively minimal, except for the heavy outflows of cash in 2020 and 2021. As we will see later, the main driver the the cash outflow in those two years were the heavy share repurchases.

Finally, looking at the change in Berkshire’s cash position shows they have not increased their cash balance cumulatively since 2018. This makes sense because BRK holds a lot of short term bonds as a substitute to cash.

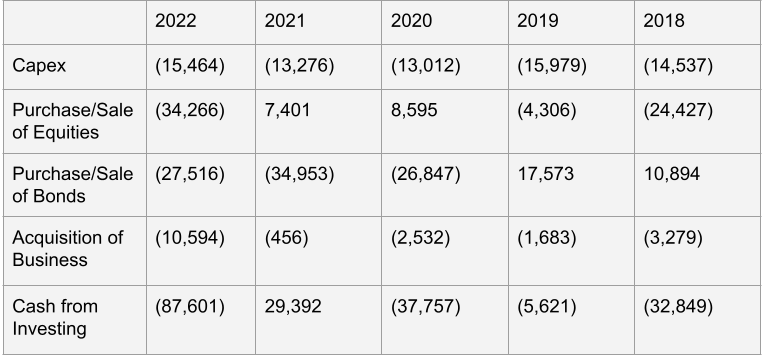

Cash for Investing

Looking at Berkshire’s cash for investing we start to get into some of the juicier bits of their capital allocation. Berkshire has been consistently spending about $15B a year on capex. As a comparison, these capital expenditures are about 40% of BRKs cash from operations. This proportion of capex to operating cash flows indicates that Berkshire is a pretty capital intensive business. Oftentimes this can be a negative, but in BRKs case, much of this capex is being spent on the railroads and utility businesses. Buffett has spoken a lot in recent years about how Berkshire Hathaway Energy has a large runway for utility infrastructure growth projects that also provide tax benefits, which is where a lot of this capex spend is going towards.

The next line item is the purchase and sale of equities, obviously an important aspect of Berkshire. Buffett put a large amount of cash towards equities in 2018, then investing $20B less in the following year. In both 2020 and 2021 BRK net sold stocks. Finally, in 2022 Berkshire spent $34B in purchasing equities, which is about as much as their cash from operations.

In 2018 and 2019, Berkshire was generating cash from the sale of their fixed income portfolio. This changed in the last three years with BRK purchasing around $30B a year in bonds. With Berkshire’s insurance operations, they have to hold a decent amount of bonds. My guess is as the insurance companies write more policies, much of that cash goes towards the fixed income portfolio.

Berkshire is also known for acquiring businesses. Each year the spend a couple billion in acquisitions. Last year was a bigger year in terms of acquisitions, with Berkshire spending $10.5B. The main acquisition in 2022 was the purchase of Allegheny Corp, an insurer.

Cash from Financing

Berkshire is interesting in that they separate the issuance of debt into two lines on their cash flow statement. The first line item is the change in debt from insurance and other businesses. These business segments paid down about $5B in 2018, but have issued $12B in debt in the last four years.

The railroad and utility segments have issued a few billion in debt each year, issuing about double that in 2020. Most utilities are required by regulators to issue a decent amount bonds, which probably explains this consistent debt issuance.

In the past 5 years, BRK has generally paid down short term debt.

Since Berkshire famously does not pay a dividend, their preferred method to return capital to shareholders is through stock buy backs. Buffett does not buy back a fixed amount of stock each year, instead he opportunistically makes repurchases when he feels Berkshire stock is trading at a decent value. This explains the variability in their repurchases.

Berkshire bought relatively little stock in 2018-19, while greatly ramping up purchases in 2020 and 2021. The buybacks in these two years amounted to nearly 70% of the company’s cash from operations, which is quite a high payout ratio. Like most stocks, Berkshire share prices declined during the market panic caused by the start of Covid. While many technology and meme stock shot up in 2021, Berkshire stock must have still been a good deal to warrant the $27B in repurchases. Buybacks slowed in 2022, but Buffett was busy buying Occidental Petroleum and Chevron stock, as well as the Allegheny acquisition.

Conclusion

Most businesses can have their capital allocation summarized by looking at a couple of line items on the cash flow statement, where Berkshire is busy allocating their capital in a variety of ways. Berkshire consistently spends around $15B a year on capex, most of this is probably growth capex. Next, Berkshire and Buffett are known for their stock picking and we can see the cash being deployed quite heavily into equities in 2018 and 2022. The fixed income portfolio is active, but this is likely due to the needs of the insurance companies. Finally, Berkshire opportunistically allocates a large portion of cash to share buybacks when Buffett thinks the stock is at a reasonable price. Warren Buffett is probably the greatest capital allocator to ever exist, so it was great to get a quick look at how Berkshire Hathaway is investing its cash flows.