A Turbocharged Value Stock

Garrett Motion is an auto parts manufacturer trading at a 40% discount to fair value with strong cash flow

A few weeks ago I wrote about Garrett Motion (GTX) and thought the stock looked interesting, even though it had some warts. When I initially looked at GTX, my main concerns were negative equity value, fairly large debt balance, and the potential for the company to do poorly during a recession. After digging deeper I became more reassured with these issues, and I layout my reasonings below. I also wanted to summarize Garrett’s recent capital allocation choices since I believe that is an important aspect to owning a stock. Finally I performed a valuation on GTX and from my estimates the stock looks quite undervalued.

Business Description

Garrett Motion is a leading supplier of turbochargers, a key technology that enhances engine efficiency and performance. A turbocharger consists of two connected turbines, where exhaust gases from the engine spin one turbine, which in turn drives a secondary turbine that compresses fresh air. This denser air is then fed into the engine’s intake, increasing power output or allowing for smaller, more fuel-efficient engine designs.

Garrett serves both original equipment manufacturers (OEMs) and the aftermarket segment, supplying turbochargers for street and racing applications. Within its OEM business, the company categorizes sales into several segments, with 2023 figures showing 25% from diesel, 44% from gasoline, 17% from commercial vehicles, 12% from aftermarket sales, and 2% from other sources. The company supplies products to 60 OEMs, including nine of the ten largest light vehicle manufacturers, with its largest customer accounting for 12% of sales. Additionally, Garrett is expanding into industrial and marine applications, sectors that are slower to transition to electrification.

As for financials, Garrett experienced a 10% drop in sales for the first three quarters of 2024. However the company maintained stable gross margins, which it attributes to a flexible cost structure that allows it to scale labor in response to demand. This flexibility is driven by a significant reliance on low-cost manufacturing locations, such as China, India, Mexico, Romania, and Slovakia, which together produced 89% of Garrett’s products. Notably, only 3% of the company’s workforce is based in the United States.

Garrett places a strong emphasis on research and development, investing $150 million annually and working closely with customers to innovate. The company employs 1,500 engineers across five R&D centers and 11 engineering centers located near customers, holding 1,300 patents. It aims to introduce 10 new technology items per year and updates its product lineup approximately every three years. To address concerns over the future of internal combustion engines, Garrett is allocating 50% of its R&D budget to battery and hydrogen fuel cell components.

The company employs 7,600 permanent workers and 2,100 temporary workers, leveraging its labor model to maintain efficiency. Geographically, Garrett’s 2023 sales were diversified, with 19% coming from the U.S., 45% from Europe, 31% from Asia, and 1% from other regions. This balanced mix helps mitigate regional economic fluctuations, though recent struggles in China’s economy have impacted global vehicle sales.

Garrett currently has a market cap slightly under $2B, and is trading around $9.20 a share. As seen below, the stock has bounced around $7 and $10 the last couple of years. Even though Garrett is trading towards its upper range, it still interested me because of the low cash flow multiple and high shareholder returns announced for 2025.

Why It is Cheap

Value stocks by definition are out of favor. Before buying a stock I like to make sure I understand why the market has sold off the company. Looking at GTX, I think there are three main reasons why it is cheap: messy spin off and capital structure changes, turbocharger sales trend, and recession fears. In the following I add some context to each of these points so I can get more comfortable with these perceived risks.

Messy Capital Structure

Garrett has been neglected by investors, primarily due to the complex financial situation it inherited after being spun off from Honeywell in 2018. Upon separation, Garrett was burdened with significant liabilities, including $1.4B in asbestos litigation claims and tax obligations owed to Honeywell. Notably, the asbestos claims stemmed from Bendix, a brake line supplier that was not even affiliated with GTX. Additionally, Garrett was hit with $240M in “transition tax” liabilities from the Tax Cuts and Jobs Act. On top of these obligations, the company took on $1.57B in long-term debt after going public, bringing its total long-term liabilities to $2.84B and leaving it with a negative equity of $2.56B.

By 2020, despite having strong operational performance, Garrett decided to go into bankruptcy to eliminate its obligations to Honeywell. After restructuring, the company emerged with a new capital structure that included preferred stock. Oaktree Capital Management, the well-known distressed debt firm founded by Howard Marks, was involved in these preferred shares. By the end of 2021, Garrett had managed to reduce its long-term debt to $1.38B while increasing its paid-in capital by approximately $1.3B, improving its equity position from negative $2.31B to negative $468M.

In 2023, GTX converted its preferred shares into common stock, which required some cash payouts to preferred shareholders. As a result, debt increased by $500M, and the equity balance dropped to negative $735M. Following this conversion, Oaktree now owns 20% of GTX. I thought it was interesting that the famous distressed debt firm now owns a big chunk of the common stock.

While negative equity is typically a red flag for investors who prioritize growing book value, Garrett’s situation appears to be more of a byproduct of its complex financial restructuring rather than a reflection of weak operations. Given the history with Honeywell, these capital structure changes seem necessary rather than concerning. However, it's understandable why some investors might avoid GTX, as the bankruptcy and negative equity could give the impression of financial instability. Despite these concerns, Garrett’s core operations remain strong, though I would like to see its debt burden further reduced.

Turbocharger Trend

One of the key concerns weighing on Garrett Motion (GTX) stock is the belief that the rise of electric vehicles (EVs) will eventually render internal combustion engine (ICE) vehicles obsolete, limiting Garrett’s long-term prospects. According to industry data cited in GTX’s 10-K from S&P, turbocharged vehicle sales are expected to decline, returning to 2022 levels by 2026 as EVs gain market share. However, despite declining ICE sales, turbocharger penetration is projected to increase from 52% in 2021 to 57% in 2025 before tapering off to 51% by 2030. Meanwhile, hybrid vehicle sales are expected to grow at an annual rate of 12%, and many hybrids already use turbochargers. Additionally, hybrid technology allows turbos to function as electrical generators, which could lead to more complex and higher-value collaborations between Garrett and OEMs.

The key takeaway from these projections is that while the overall number of ICE vehicles with turbos will decline, this trend may be partially offset by more sophisticated turbocharger installations in hybrid vehicles. In this scenario, Garrett may not see significant revenue growth, but it should be able to tread water for a while. Current projections suggest EVs will make up 36% of vehicle sales, up from 19% in 2023. However, these estimates may be overly optimistic. In recent years, government policies have pushed EV adoption, and Wall Street has pumped EV stocks, yet consumer demand appears to be plateauing. Any repeal of tax incentives or delays in charging infrastructure expansion could slow adoption further. Additionally, many consumers may wait for EV technology to improve in terms of range, charging times, and affordability before making the switch.

Beyond the automotive market, Garrett is also expanding its turbocharger solutions into industrial and marine applications. While this segment is unlikely to generate substantial sales, it could help offset some of the decline in automobile-related revenue. Overall, even in a base-case scenario where Garrett sees little to no revenue growth, the company is likely to remain relevant over the next decade. As long as it continues to generate strong cash flow and return capital to shareholders, flat revenue growth is not necessarily a major concern. However, if EV adoption progresses more slowly than expected, Garrett stands to benefit further from the continued “turbo-fication” of combustion engines.

Recession Scenario

A common theme in the market over the past few years has been the punishment of stocks perceived to be vulnerable in a recession. This fear is understandable, as buying a cyclical stock only to see a downturn crush its value is not ideal. However, since predicting the timing of economic downturns is difficult, a more practical approach is to simulate a reasonable worst-case scenario and assess how the business fundamentals might respond.

In Garrett Motion’s case, historical data from its time under Honeywell provides insight into how it performed during the 2008 recession. Garrett was part of Honeywell’s “Transportation Systems” segment, which also included some consumer auto parts businesses. While these sales were aggregated in earlier years, by 2008, Honeywell began reporting turbocharger sales separately. During that period, Transportation Systems’ revenue declined from $5.0B in 2007 to $3.4B in 2009, a peak-to-trough drop of 33%. Turbocharger sales followed a similar trajectory, falling from $3.6B in 2008 to $2.4B in 2009 before rebounding to $3.9B in 2011. Despite the sharp revenue drop, the turbo segment still managed to generate $61M in profit in 2009.

Given that the 2008 recession was particularly severe, a future downturn could be milder. However, for this analysis, assuming a 30% decline from Garrett’s 2023 peak sales, revenue would fall to $2.72B. Garrett often highlights its flexible cost structure, which has allowed it to maintain stable gross margins of around 19%, even during a 10% sales decline in 2024. A key factor in this flexibility is its large portion of temporary workers. That said, assuming gross margins drop to 10% in a severe downturn, Garrett would still generate $272Min gross profit.

On the expense side, if R&D and other discretionary costs are cut, SG&A could be reduced to $200M, leaving $72M in operating income—insufficient to cover interest expenses. However, on a cash flow basis, reducing capital expenditures and adding back $90M in depreciation would result in approximately $162M in EBITDA, which would mostly cover Garrett’s interest obligations.

Ultimately, Garrett has already demonstrated its ability to maintain strong cash flow even with a 10% decline in sales since its 2023 peak. If the company aggressively cuts discretionary spending and maintains a reasonable gross margin, it should be able to navigate a challenging economic environment for a year or two. While a downturn would likely cause the stock price to suffer (frustrating for current investors) it could also present a buying opportunity for those willing to wait for an eventual economic rebound.

Financials

Garrett Motion’s income statement over the past five years reflects relatively stable performance, with revenue hovering around the mid-$3B range. The company experienced its weakest year in 2020 but reached a peak in 2023 before seeing a roughly 10% decline in sales in 2024. Despite these fluctuations, gross margins have remained steady at approximately 19%, demonstrating the resilience of Garrett’s cost structure. Operating income has consistently hovered around $500M, with the exception of 2020, when lower revenue and gross margins weighed on profitability.

One notable trend is the rising interest expense over the past two years, which coincides with the broader increase in interest rates since 2022. Last year, depreciation expense totaled $90M, closely aligning with Garrett’s capital expenditures, indicating that the company is reinvesting to maintain its asset base. In terms of returns, Garrett has consistently delivered a return on assets (ROA) in the low double digits, with the latest trailing twelve-month (LTM) figure at 12.6%. This suggests the company is generating returns above its cost of capital, which is a positive sign.

On the balance sheet, debt remains a key consideration. Since Garrett has negative equity, a debt-to-equity ratio is not meaningful, but its debt-to-EBITDA ratio stands at approximately 2.2x. While not not at private equity levels high, it is higher than I would prefer for a auto parts manufacturer. Another noteworthy point is that Garrett’s net property, plant, and equipment (PP&E) is currently valued at $450M, despite originally costing $1.5B. This raises the question of what the true replacement value of Garrett’s fixed assets might be.

Overall, Garrett’s income statement reflects strong earnings potential, with stable margins and solid profitability. However, it would be beneficial for the company to reduce its debt and interest expenses to strengthen its financial position further.

Capital Allocation

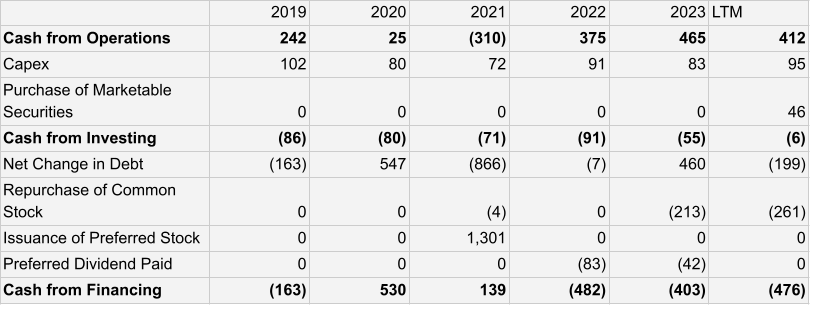

Garrett Motion’s capital allocation decisions are best analyzed through its cash flow statement, which provides insight into how the company manages its resources. Over the past five years, cash flow from operations has fluctuated significantly, peaking at $465M in 2023 while hitting lows of $25M in 2020 and negative $310M in 2021. The latest twelve-month (LTM) figure stands at $412M. The weak cash flow in 2020 was likely influenced by bankruptcy-related factors, while 2021 saw restructuring costs weigh on results.

Capital expenditures have remained relatively stable, ranging between $80M and $100M annually. The LTM capex figure was $95M, representing about 23% of operating cash flow. On average, GTX spends roughly 25% of its operating cash flow on capex, which is relatively capital-light for a manufacturing company. Aside from capital expenditures, Garrett hasn’t made any other significant investments in the cash flow from investing section.

Cash flow from financing activities has been more volatile due to frequent debt issuances, repayments, and preferred share transactions. Since 2019, Garrett has reduced its total debt balance by $220M, a prudent move given its leverage. While the company repurchased $213M worth of common stock in 2023, this was part of the preferred-to-common stock conversion. However, in the first nine months of 2024, GTX repurchased $226M in shares, its first true shareholder return since the spin-off. Previously, the company had only paid preferred dividends, with no common dividends.

Recently, Garrett announced its capital allocation plan for 2025, aiming to return 75% of free cash flow to shareholders. This includes a $50M regular dividend and up to $250M in share buybacks. The transparency in communicating this plan is a positive development. Overall, Garrett appears to allocate capital efficiently, reinvesting modestly in capex while prioritizing debt reduction and shareholder returns. Establishing regular shareholder distributions should help GTX move past its complex restructuring history and potentially attract more investor interest.

Valuation

Despite the complexities of its past reorganization, Garrett Motion remains consistently profitable, with a return on assets above its cost of capital. Given this stability, an earnings power valuation (EPV) approach seems appropriate. This method estimates a reasonable net operating profit after tax (NOPAT), capitalizes it at the company’s cost of capital, and then adjusts for debt and cash to determine the equity value.

Starting with a five-year average operating income of $455M and applying a 25% tax rate, we get an estimated NOPAT of $341M. To estimate the cost of capital, I assume a 50/50 debt-to-equity split while adjusting the cost of debt for tax savings. With GTX holding a BB- credit rating, debt yields are around 6%. Meanwhile, the Vanguard Small-Cap Value ETF carries a price-to-earnings ratio of 16x, which seems somewhat high. Given GTX’s market cap and overall business quality, I estimate a 9% cost of equity. This results in a weighted average cost of capital (WACC) of 6.75%.

Using this WACC, dividing NOPAT by 6.75% produces an enterprise value estimate of $5,050M. After adding $90M in cash and subtracting $1,475M in debt, the estimated equity value comes out to $3,675M. With 231.02 million shares outstanding, this translates to a fair value estimate of approximately $15.90 per share.

With Garrett currently trading around $9.20, this valuation suggests the stock is significantly undervalued relative to its intrinsic value.

Conclusion

In summary I believe Garrett is quite undervalued and I have started buying some shares. It makes sense that investors would be scared off by Garrett’s recapitalizations and industry dynamics. However after looking deeper into these, I think I can get comfortable with these risks. It wouldn’t be a value stock if it didn’t have some warts. GTX reports its full year 2024 results soon, so we shall see if sales have picked back up or if the industry downturn continues.

Stocks mentioned: GTX 0.00%↑

Great analysis!