Enterprising Investor at a Glance

Later this week I will be out in Omaha for the Berkshire annual meeting, which will I’m sure I will have a great time hanging out with fellow value investors. Since investing is not my day job, I don’t get much practice pitching my stock ideas or investing strategy to people. I thought I better put together some talking points to be better prepared, and figured I would turn it into a little Substack post. The added benefit is that I have recently gained a decent amount of subscribers, so this post could be helpful for the newbies to get up to speed on some of my investing thoughts.

Investment style in brief: I invest in out of favor companies trading below their fair value. I focus on small companies, however I do own a couple larger market cap stocks like Dollar General and British American Tobacco. In general I’m trying to replicate Buffett’s partnership years.

YTD return: 1.75%

Number of holdings: 11 major, 6 minor/special situations

Top 5 largest holdings current market value: DG, GTX, BTI, TLF, NLOP

Top 5 largest holdings by cost: TLF, GTX, NLOP, DG, JCTC

Current top 3 largest gains: HIFS 39%, MPAA 79%, DG 25%,

Recent big winners: COF 190%, SPG 130%, SENEA 80%, MPAA 79%

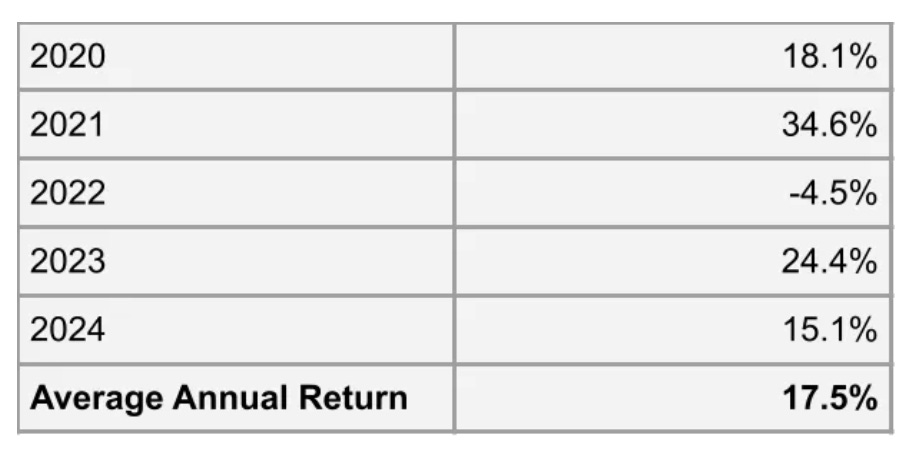

Five Year Track Record

Current Holdings

Notable Positions

Garrett Motion (GTX)

Story

Messy balance sheet from Honeywell spinoff, bankruptcy to get rid of legacy Honeywell asbestos liabilities, post-bankruptcy recapitalization

Fears of combustion engines being obsolete

Recession fears

High free cash flow generation

I’m not pessimistic about EVs making turbochargers obsolete

New capital allocation strategy

Key Metrics

Market cap: $1.87B

Sales decline, look for rebound: previous quarters sales down 10% YoY

Gross margins holding up: hovering around 20%, last quarter was 21.6%

FCF: $317M in 2024

New Shareholder return plan: $50M dividend, up to $250M in buybacks, 75% of FCF returned

Current gain: 4%

Valuation

NOPAT $341M, 6.75% cost of capital, $3.675B equity, $16 a share fair value

Dollar General (DG)

Story

Was a growth stock, growth slowing, saturated markets could limit new store openings

Decline in margins due to shrink, increased labor, distribution, store opening costs

Low income consumer more heavily impacted by inflation, focusing on lower margin consumables instead of higher margin products

Current valuation seems attactive even if growth is mediocre

Inflation pressures will eventually subside so margins should revert closer to historical levels

Key Metrics

Recovery in gross and operating margins: assume operating margins get back to 7%

Same store sale growth: hopefully better than 0.5% from a recent quarter

Shareholder returns: $518M in dividends, about 20% of operating cash flow, used to do buybacks when stock was high but did none in 2024

Current gain: 25%

Valuation

NOPAT $2.22B, 6.7% cost of capital, $27.3B equity, $124 a share fair value

Motorcar Parts of America (MPAA)

Story

Car parts suppliers out of favor, cyclical, obsolete from EVs

Earnings sensitive to exchange rates, increased interest expense from receivables financing plus new preferred stock

Replacement altenators are not tied to new vehicle sales, and can not be a delayed purchase by customers

Expanding product offering with brake parts

Auto parts retailers have been expanding their merchandise to increasingly include MPAA products

Net income should improve if interest rates decrease or company reduces revievables financing balances

Key Metrics

Market cap $179M

Look for interest expense to decrease

Revenue up 8%, gross margins up 6.5%, need to flow down to net income

LTM FCF $24.8M

Could be doing up to $16M in buybacks

Current gain: 79%

Valuation

Fair value is around book value, which is $13