Capital Allocation Snapshot: Tractor Supply

Tractor Supply is a retailer that caters to rural activities like farming, lawn care, pet care, and home goods. Many retailers are not very good businesses, but Tractor Supply has carved out a unique niche that makes them one of the strongest retail companies. Tractor Supply has a market cap around $24B, has a great record for stock appreciations, and has generated nice profits. In this post, I will summarize Tractor Supply’s cash flow statement to get an idea of how they allocate their capital.

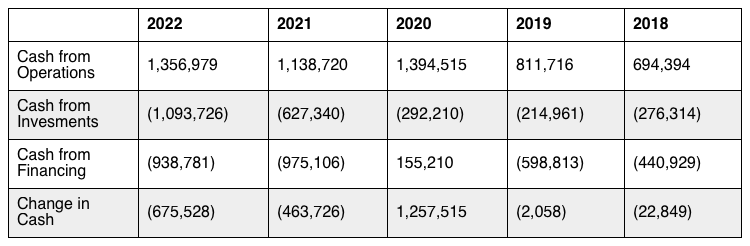

Cash Flow Summary

Tractor Supply’s cash from operations started off around $800M during 2018 and 2019. Then in 2020, the company’s cash flow increased to nearly $1.4B. This value dipped a bit in 2021, but rebounded to $1.3B in 2022. These figures show a nice growth in TSCOs cash from operations over the period, but it would be good to understand why the big increase in 2020 then the subsequent plateau.

From 2018 to 2020, Tractor Supply’s cash from investments ranged between $215M and nearly $300M. The spend on investments doubled in 2021, then dramatically increased again in 2022.

Tractor Supply’s cash from financing varies widely over the period. The first couple of years showed TSCO having around $500M in cash outflows. Cash from financing produced cash inflows during 2020. Then in the last two years, Tractor Supply has spent almost $1B a year on financing.

Finally, looking at the net change in cash shows the TSCOs cash balance has practically remained unchanged over the last five years.

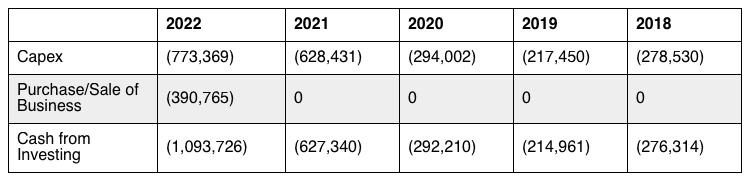

Cash from Investing

Turning to Tractor Supply’s cash from investing, we see the two main line items are capex and the purchase of a business. TSCO spent around $300M on capex in 2018 through 2020. Then capital expenditures doubled in 2021 and 2022. The increase in capex is due to Tractor Supply opening new stores and upgrading some existing stores.

In 2018, nearly half of cash from operations was used to fund capex. This ratio decreased the next few years as capex remained constant but cash from operations increased. The last couple of years, Tractor Supply has reached the 50% ratio again with the elevated cash from operations and increased capex spend. These periods with the elevated capex to cash flow ratio seem to indicate TSCO is fairly capitally intensive. A counter to this is that the expense is probably more for growth opposed to maintaining current operations.

As for acquisitions, in the last five year Tractor Supply has only made a single purchase. In 2022, TSCO spent $390M in acquiring Orscheln, a competing farm and home retailer. Since Tractor Supply’s market capitalization is around $24B, this is a small acquisition that should not affect the overall business too much

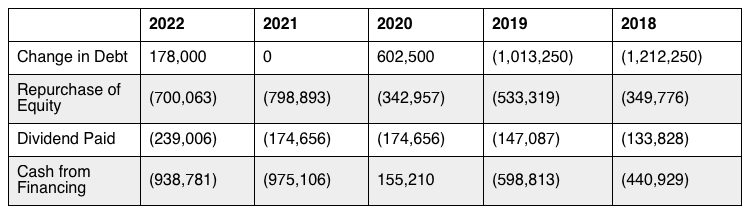

Cash from Financing

The first line item in Tractor Supply’s cash from financing is the change in debt. For the first two years in the period, TSCO paid down $2.2B in debt. The following year saw debt increase by $600M, and a bit more debt was issued in 2022. Tractor Supply’s D/E is 0.83, and D/EBITDA is 1.0. These values are pretty low, meaning TSCO is not over indebted.

Next we get to shareholder returns. Tractor Supply did around $350M in share buybacks in 2018 and 2020, while bumping this figure up to $530M in 2019. Share repurchases peaked in 2021 at nearly $800M, then decreased by $100M in 2022. Except for 2020, Tractor Supply has typically used around 50% of their cash from operations to buyback shares.

The next avenue to return cash to shareholders is through dividends. TSCO has steadily increased their dividend, although it remained flat from 2020-2021. Over the last five years, Tractor Supply’s dividend has hovered around 15% of their cash from operations. Clearly, Tractor Supply favors share repurchases to dividends, but still tries to keep a consistently growing dividend.

Adding the dividends to the buybacks, TSCO is returning about 65% of their profits to shareholders. This payout ratio is fairly high, and would be sound capital allocation for a mature low-growth company. However, since TSCO is also spending a large portion of their operating cash flow on capex to grow, it sends mixed messages. If a company can achieve high returns on investment through internal growth opportunities, then they should focus on allocating capital there instead of returning cash to shareholders.

Conclusion

Tractor Supply generates a healthy amount of cash flow from operations that has generally grown in the past five years. The company has allocated this capital primarily in two ways. First TSCO has been spending nearly 50% of its cash flow on capital expenditure, which mostly involves opening and renovating stores. Second, the company has returned over 50% of its profits to shareholders, mostly through buybacks, but also with a decent dividend. Tractor Supply has not made many acquisitions over the last five years, but did use a decent chunk of the years cash for operations to buy a smaller competitor.

My observation is that Tractor Supply is trying to grow its business through opening stores, and acquiring competition, but on the other hand is returning a lot of cash to shareholders. I believe the optimal capital allocation strategy would be to reinvest profits within the business if there is are good returns from opening stores. Returning cash to shareholders should be a last resort, if there are no other good investment opportunities. However, maybe there is some limiting factor that prevents Tractor Supply from deploying all of their profits into new stores each year. Further study on the company’s capex and store growth would need to be done.