Capital Allocation Snapshot: Occidental Petroleum

Continuing with this months theme of large Berkshire Hathaway stock holdings, this week I am profiling Occidental Petroleum (OXY). Warren Buffett has been aggressively buying shares of OXY over the past year, with Berkshire owning about 20% of the company. In this post I will summarize Occidental’s cash flow statement to get an idea of how they are allocating capital.

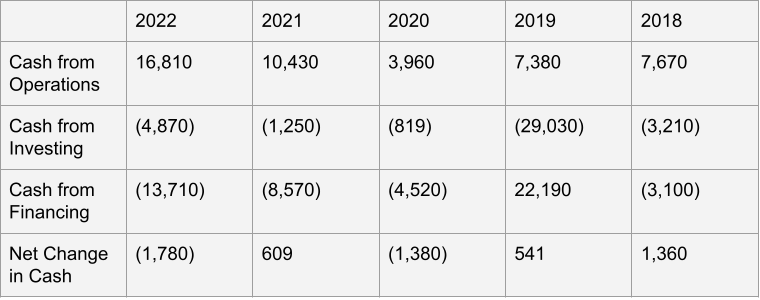

Cash Flow Summary

Let’s get started by summarizing Occidental’s cash flow statement. Cash from operations in 2018-19 were both around $7.5B, then got cut in half in 2020. Don’t forget that the price of oil declined greatly in 2020 with the lack of demand due to Covid. Cash from operations strongly rebounded in 2021, and 2022 cash flow is more than double pre-pandemic levels.

OXY’s cash from investing is usually a few billion a year, except for the $29B spend in 2019. We will get into this more later, but in 2019 Occidental made a large acquisition, buying Anadarko Petroleum.

As for cash from financing, Occidental had a large inflow of cash in 2019 in order to fund the acquisition. The other years have seen OXY generally increase their spend on financing.

Over the last five years, Occidential’s cash balance has not really increased.

Cash from Investing

One area where a company can reinvest in its business is through capital expenditures, ideally this spending produces a good rate of return. Prior to 2021, OXY was spending between 65-85% of its operating cash flow on capex. In the last two years, this figure has been around 30%. Without looking into the details, it is hard to say what a long term average capex spend is. Another factor is that typically there is maintenance capex, just to keep the business going, and growth capex. More research would need to be done to get an idea how much of Occidental’s capex is for growth.

On the acquisition front, OXY made the $55B acquisition of Anadarko Petroleum, although only $28B of the purchase was with cash. Interestingly, Berkshire Hathaway provided financing for this deal. Buffett contributed around $10B in exchange for OXY preferred stock and warrants. As for the other years, Occidental has been making smaller acquisitions and investments that make up a few percentage points of their operating cash flow.

To offset some of these acquisitions, OXY has been selling assets. Part of the deal with Anadarko was to sell off some of their assets. Occidental has sold off oil assets in the Permian basin, Ghana, and it seems like they have many joint ventures.

The other line item seems pretty insignificant.

Cash from Financing

As expected, 2019 had a big increase in debt for Occidental. The last three years has shown the company pay off debt, with 2021 and 2022 payments offsetting the $15B increase in 2019.

Usually you don’t want to see a company issue stock unless its for a good reason. OXY raised $10B worth of equity in 2019 to fund the big acquisition. Provided the the purchase of Anadarko was a good deal, the issuance of equity could be beneficial for OXY shareholders. If OXY overpaid or something, then obviously the issuing of stock would make the problem feel worse to shareholders that got diluted.

Since Occidental was busy buying Anadarko, the period 2019-2021 they did not repurchase any shares. In 2022 they made their largest buyback, spending over 18% of operating cash flow on buybacks. Granted 2022 had elevated cash from operations. Buffett has been acquiring a large chunk of OXYs stock over the past year. He stated part of his rationale is that Occidental is going to be smart about returning capital to shareholders instead of over-investing in drilling for oil. As seen in the recent past, as oil prices increase, US oil drillers get on a bonanza spending a bunch of money in drilling for oil, which causes a glut and prices to tumble.

Occidental’s dividends grew from 2018-19, but then decreased quite a bit the following two years. The company slightly increased the dividend again in 2022. With Occidental’s dividend payout varying so much, its hard to get a read on a typical payout ratio. In 2019 they spent about 30% of cash from operations on dividends, 50% in 2020 and only 7% in 2022.

Conclusion

Some of the main take aways from Occidental’s capital allocation is their heavy capex spend. This could be a good capital allocation decision if the oil wells, pipelines, storage facilities, or whatever produce an attractive rate of return. Or bad if these items produce a low rate of return. The next big allocation move was the acquisition of Anadarko. Once again this could be a good decision of the acquisition produces a good return on investment and if operating costs can be reduced. Since the acquisition, OXY has spent a lot of their cash flow in paying down debt, which is probably a good idea.

When it comes to returning capital to shareholders, Occidental has leaned in to buybacks last year, spending more cash on that than their dividend. The dividend payout is pretty low. In the last five years, it does not appear OXY has focused on returning capital to shareholders, they have been spending money on growing the business instead. With a large portion of their debt paid down and sizable buyback last year, perhaps Occidental will focus their capital allocation on returning cash to shareholders going forward.