Capital Allocation Snapshot: Monarch Cement

Often times with these Capital Allocation Snapshots, I choose a company to profile that is interesting or different. This week I am taking a look at Monarch Cement, a microcap stock with market capitalization around $340M. Monarch mainly manufactures portland cement in Kansas, Iowa, Missouri, and a couple of other states. I like Monarch Cement because it seems like a simple business and is a high quality microcap company where most stocks of this size are not of high quality. In this post I will take a look at Monarch’s cash flow statement to get an idea of how they allocate their capital.

Cash Flow Summary

Starting out with Monarch’s cash from operations, we see rather large step ups in cash flow from 2018 to 2019, then again from 2019 to 2020. After 2020, Monarch’s cash flow has hovered around $50M. Since the company is in the basic materials sector, it would make since that their profits will be cyclical, but we would have to go back to 2008 to see how cyclical monarch is.

In most years MCEM spends about $20M a year in investments. The outlier was in 2021, where the company only spent $6M.

Cash from financing has ramped up, going from $7.5M to $12.9M in 2020. Then in 2021, financing spent doubled to over $24M where it has remained since.

Over the last five years, Monarch has consistently built up their cash balance. The outliers are 2018, where Monarch’s cash balance dipped a bit. On the other end, in 2021 Monarch had a large increase in cash at $23M.

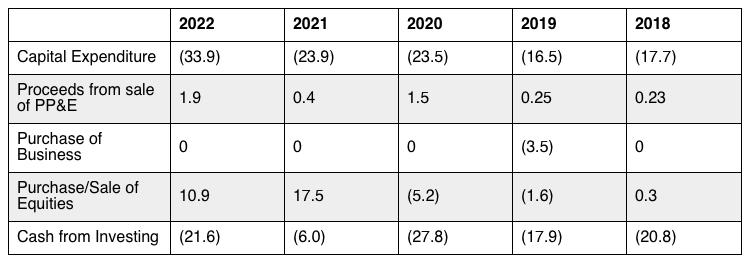

Cash from Investments

Turning to Monarch’s cash from investments, we can begin to see where they allocate capital. A large portion of Monarch’s cash from investing goes towards capital expenditures. This figure has been ramping up over the last five years, starting around $17M in 2018-19, bumping up to $24M in 2020-21, then increasing again to $34M in 2022. During most years, this capex level is about 50% of MCEM’s cash from operations. I am sure cement plants wear down heavy machinery pretty quickly, so it makes since that Monarch would be a moderately capital intensive business.

The next line item in Monarch’s cash flow statement is the proceeds from sale of property, plant, and equipment. Their annual report does not specify what exactly is being sold. However, this value is pretty small, but it is interesting the company is constantly selling equipment.

Acquisition of businesses is an important capital allocation decision. With Monarch we see that they have only made a single $3.5M purchase in 2019. The purchase of this business represents about 1/10th the market capitalization of MCEM, so this acquisition is probably inconsequential.

The last line item in the cash from investment section is interesting because Monarch is active in buying and selling equity securities. During 2019 and 2020 Monarch on net, invested a total of $6.8M in stocks. The latest two years shows Monarch selling quite a bit of their stock portfolio, generating $17.5M in cash in 2021 and almost $11M in 2022. At the end of 2022, Monarch’s stock portfolio amounted to $42M. These proceeds from the equity sales are about 30% the company’s cash from operations.

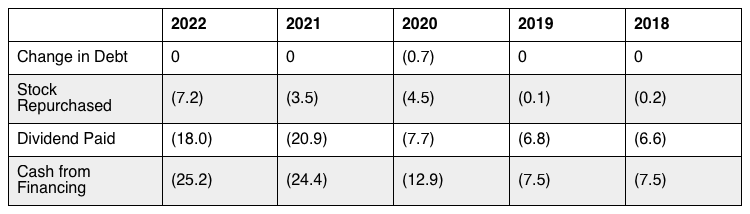

Cash from Financing

Monarch’s cash from financing section is pretty straightforward. The only financing move the company was to pay off $750k worth of debt in 2020.

The rest of Monarch’s cash from financing is cash returned to shareholders. MCEM did not repurchase much stock in 2018-19, but they did cumulatively buy $7.5M from 2020-21. Then in 2022 the company step up their repurchases to over $7M. I believe Monarch usually trades at a reasonable valuation, so it is likely these stock buybacks are moderately beneficial to shareholders.

Monarch returned more cash to shareholders via dividends. The company paid a bit over $6.5M in 2018 and 2019, then raised the dividend by nearly $1M in 2020. Over the past two years, Monarch has significantly increased their dividend to around $20M a year. Comparing total shareholder returns to cash from operations, Monarch was returning about 30% of profits during 2018-2019. Lately they have increased their payout to around 50% of cash flow.

Conclusion

Monarch Cement is a pretty simple business, and their cash flow statement was enjoyably simple to read. Over the past five years, Monarch has generated a growing amount of cash from operations. The first main capital allocation move Monarch makes is to reinvest about half of their cash flow into capital expenditures. Next, Monarch maintains an equities portfolio that is the destination of some of their cash, and also a source of cash flow when they sell securities. The last main capital allocation move Monarch makes is to return most of the remaining cash flow to shareholders. These shareholder returns have dramatically increased lately, with MCEM increasing their dividend and beginning to do share repurchases. Overall, I would say Monarch Cement has a reasonable capital allocation policy.