Capital Allocation Snapshot: Meta

In this weeks Capital Allocation Snapshot I am looking at Meta. Meta is an $805B company, but for a while the stock sold off quite heavily due to the perceived competition with TikTok and heavy spend on the metaverse. After being a value stock for a while, Meta has greatly recovered in market cap. With Meta being a good example of a large stock that can temporarily go out of favor, I thought it would be interesting to take a look at their capital allocation.

Cash Flow Summary

Over the past five years, Meta has increased their cash from operations by about 67%. The lowest figure came in 2018, then by 2021 Meta doubled their cash flow. Then in 2022, Meta’s cash from operations dipped a bit, coming in at $50.5B. It will be interesting to see if Meta’s profits continue to decline like 2022, or if that is a blip on the impressive five year growth figure.

Next is Meta’s cash from investing. In most years, the company has spent quite heavily on investments. The investment spend in 2018 and 2021 came in a bit lighter than the other years, hovering closer to $10B. The other recent years showed Meta spending $20-30B a year, which is a pretty high percentage of their cash from operations in those years.

Meta’s cash from financing varies even more than the company’s cash from investing. Each year, Meta is spending cash on financing, which means they are returning cash to shareholders. The years 2019 and 2020 saw Meta spend relatively little in cash from financing, while this figure increased by a factor of five in 2021.

Looking at Meta’s net change in cash over the last five years shows that the company built up its cash balance in 2018 and largely in 2019. The last three years saw Meta draw down its cash balance.

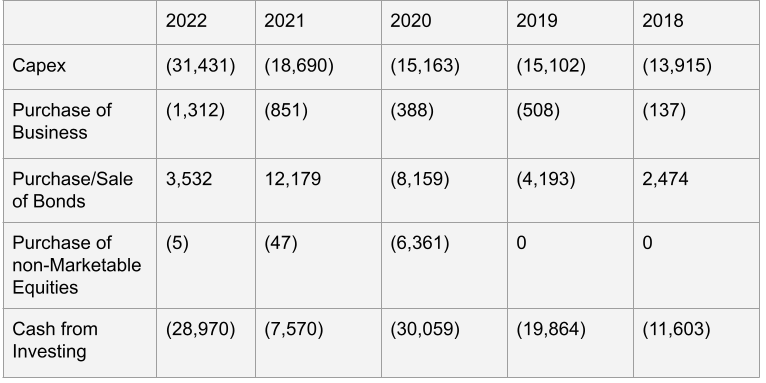

Cash from Investing

Now turning to Meta’s cash from investing, we can start to see how they allocate capital. From 2018-2021, the company has spent around $15B on property and equipment. This figure nearly doubled in 2022, which is potentially explained by investments into hardware for metaverse development. For the most part, Meta has spent around 40% of its cash from operations per year on capital expenditures. This is a bit surprising to me, since Meta is known for the social media apps I figured they would not be very capital intensive. My guess is that much of this capex spend is on servers and other high end computing equipment.

The next line on Meta’s cash flow statement is the purchase of business. Each year in the last five, Meta has acquired some business. The spend for these businesses range from $130M-$1,300M, which is quite insignificant compared to Meta’s $800B market capitalization. Acquisitions can be a major capital allocation decision, but in Meta’s case, these small purchases will not move the needle much.

Meta invests some of its cash into fixed income securities. Each year the company is selling some of its bonds, while buying new bonds or having some bonds mature. In 2019 and 2022, Meta allocated $12B towards fixed income securities. While in the last two years, the company gained $15B in cash from selling some of its bonds. Investing in bonds is better than earning no yield by sitting in cash, however bonds do not have a high rate of return. This means that if Meta does not eventually put this cash to better use, it could be an inefficient use of capital.

The next line is atypical, with $6B being spent on the purchase of non-marketable equity investment.

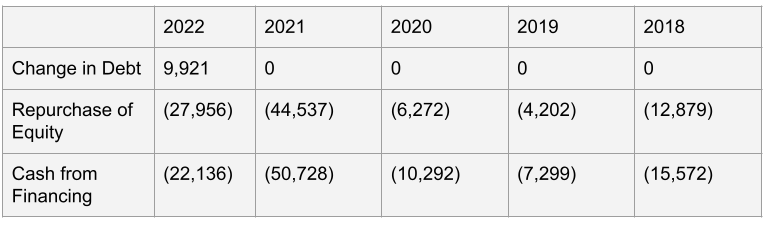

Cash from Financing

Over the last five years, the only time Meta issued debt was in 2022. At the end of 2022, Meta had $25.2B in debt compared to an equity value of $125.7B, resulting a D/E ratio of 0.2. Looking at debt-to-EBITDA, the company had a value of 0.67. Both of these debt metrics show that Meta has very little debt burden.

Next we can look at how Meta returns cash to shareholders. The company does not pay a dividend, but it does consistently repurchase its stock. The stock buyback figures vary quite a bit, low points being around $5B in 2019 and 2020. The peak buyback spend was in 2021 at $44.5B, then repurchases declined a bit to $28B the following year. For context, the buyback in 2021 amounted to 77% of Meta’s cash from operations, and 55% in 2022. This ratio was only 11.5% in 2019.

This wide range in buybacks seem to indicate that Meta is opportunistic in their buybacks, instead of a constant return of cash to shareholders. It would be interesting to look at Meta’s share price in 2021 to see if the company was overpaying for buybacks during that year. On the other hand, the company’s stock sold off heavily in 2022, so those buybacks may turn out to be very lucrative to the existing shareholders during that period.

Conclusion

During the last five years, Meta has steadily grown in cash from operations. The company has reinvested a decent chunk of these profits into capital expenditures. Further research could be done to see what type of property or equipment Meta is investing in, but my guess it is largely high end computers. Meta invests some of its cash into bonds, which probably isn’t the most efficient capital allocation move but may allow the company to weather a rainy day or make a strategic acquisition. The final main capital allocation move from Meta is the repurchase of its stock. Repurchases were comparatively low in 2019 and 2020, but have dramatically ramped up the past couple of years. Buying back stock can be a good capital allocation decision as long as the management is not over-paying for the stock.

I think META is underrated in capital allocation. Zuck’s made smart acquisitions and plays the long game (WhatsApp) and never sold his voting rights for some capital raise. What got my attention is the only equity comp they pay is RSUs (restricted stock). No stock options.