2023 Portfolio Update

Performance Overview

My portfolio of individual stocks was up 10.0% in Q4, and produced a gain of 24.4% for the full year. The starting balance of the portfolio at the the beginning of the year amounted to $75,407 and ended the year at $105,214. Contributions to this portfolio for the full year amounted to $11,873.

The annual returns of my stock picking portfolio since I started publicly sharing my portfolio are shown below.

Year In Review

At the time of this writing, in late December, it is hard to believe that there was a major banking panic earlier in the year. So far, it appears the ripples from the failures of Silicon Valley Bank, First Republic, and Signature Bank, have not broadly impacted the financial system or stock market. Throughout much of the year, commentators speculated that regional banks would be the next shoe to drop. It was feared the regional banks would lose deposits to the Too Big to Fail Banks. Also regional banks banks could be under pressure by seeing withdrawals to alternatives such as money market funds and Government bonds since these finally have some yield. The ETF that holds regional bank stocks is down about 12% for the year, but for much of the year it was hovering around a 35% loss.

All banks would love to see their deposits increase, and a 5% increase in deposits would be considered quite nice. Looking at SVB, deposits were about $50B in 2018. The amount of deposits then quadrupled to around $200B in Q1 of 2022. Then, as interest rates increased throughout 2022, SVB’s deposits slid down to $175B by the end of the year.

The reason for this growth was that SVB was focused on primarily the Silicon Valley region, meaning that many of the tech start ups, IPOs, venture capital funds, private equity, SPACs were based in SVB’s back yard. These types of funds and companies went through a speculative mania during 2020-2021. As these funds were deploying capital, and the start ups absorbing the capital, they deposited their cash into Silicon Valley Bank.

The first problem with SVB is that they need to do something with all this cash coming into the bank. Ideally, a bank would like to make loans with its deposits, but that takes time. Instead, Silicon Valley Bank bought Government bonds to provide some yield on all this cash. This is not too bad of a decision on its own, but SVB decided to primarily buy long duration bonds instead of short duration. Long duration bonds provide a little bit more yield, but you are more exposed to the effects of interest rates. Buying long duration bonds probably is not that bad of an idea in most times, but SVB happened to buy a large amount of these bonds right as inflation began to rise. The increase in interest rates due to inflation destroyed the value of SVB’s bond portfolio, badly weakening the company’s financial health.

The massive paper losses in SVB’s bond portfolio set the bank up for potential failure, but it is possible that the bank could have waited things out. If interest rates fell back down, then the crisis would be avoided. Compounding the issue for SVB was the outflow of deposits due to alternatives providing higher yields. While financial analysts and regulators were sleep walking into this crisis, it was SVB’s own clients that killed the sickly bank by gossiping about the banks weakness in March 2023. Aided by social media, there was a flurry of comments that SVB was in trouble and that everyone should pull their cash out. This is the setup for the classic bank run, causing SVB to fail.

The collapse of Silicon Valley Bank can be summarized as a string of poor decision making that put the bank on a weak footing. I believe the bank regulators and stock analysts should have seen the warning signs sooner, but instead we got a bank failure. While I am focusing on Silicon Valley Bank, the other banks that failed were similarly weak as SVB, and were victims of the panic.

As the crisis was unfolding, I was sitting at the edge of my seat hoping to buy some bank stocks at a discount. Most banks did selloff quite a lot, but not to the once in a generation valuations seen during the 2008 financial crisis. That being said, I still purchased shares of Hingham’s Institute for Savings at a book value far below average, and I bought some Bank OZK preferred shares that yield around 8%.

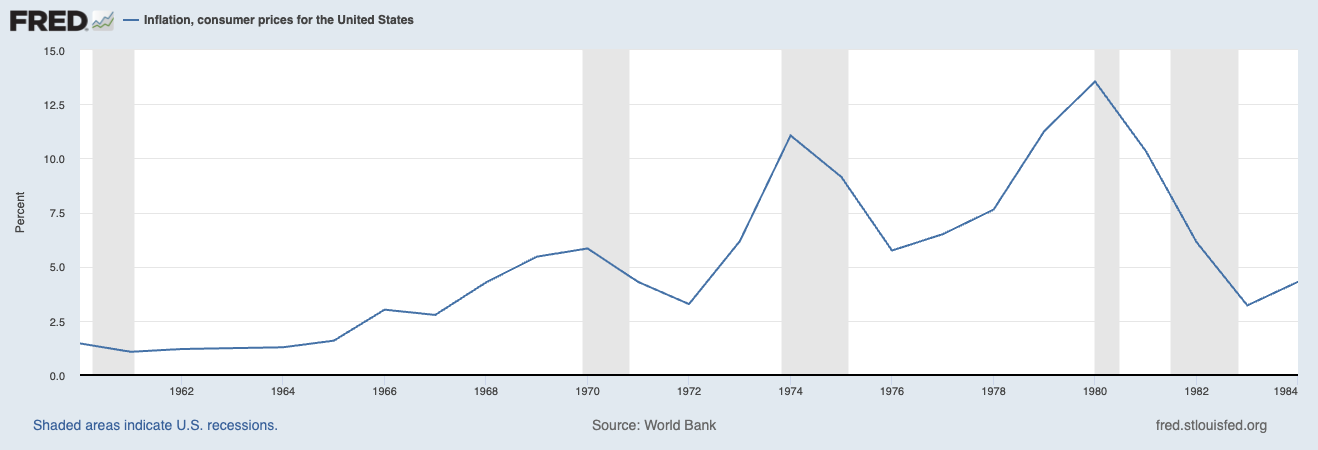

For the past couple of years, inflation has been one of the main themes in finance. During the last year, the year-over-year rate of price increases has slowed. In January the yearly change in inflation was 6.45%, in November it was 3.14%, and for context the rate peaked at 9.06% in June 2022. Looking at purchasing power, the change in CPI for the year was about 2.5%. Since January 2020, purchasing power has decreased nearly 19%. The consensus among Wall Street is that interest rates will significantly decline next year, which would be good for both stocks and bonds.

I dare not make a prediction on what interest rates will be next year, but I think it can be useful to think through the different scenarios. The first is the “soft landing” where interest rates come down and the economy hums along just fine. The second is a recession, which has been predicted to happen for over a year now. This recession could materialize, which would cause lower interest rates, but stocks probably would not fare well. Then there is the possibility that inflation picks back up. Looking at the figure below, we see that during the last inflationary period there were several instances where CPI peaked, declined, then started to rise again. I do not want to sound too pessimistic, but I want to be cautious and mentally prepared for any scenario.

Turning to my portfolio, this year saw me somewhat inadvertently position myself to be short interest rates. Holdings such as British American Tobacco, Verizon, and Bank OZK preferred were purchased for their high dividend yield. While not the sole reason, but a large reason why these stocks have sold off the past year or so is due to interest rates increasing. Higher interest rates meant that investors can get a safe yield in low duration bonds instead of buying stocks known for their dividends. Another factor causing British American Tobacco and Verizon to trade at low prices is that they have pretty heavy debt loads. As their current debt matures, these companies will have to refinance with higher interest rates, which will hurt their earnings.

The reason why I like BTI and Verizon is that I believe they have pricing power during an inflationary environment. If inflation continues, I think these stocks would still perform fine. However if rates do fall next year, I think the prices of these stocks can rally back to where they were a few years ago. In my head, this seems like a “heads: I win, tails: you lose” scenario, but we will wait and see how it pans out.

This year I only added five substantial new positions, and added to two existing holdings. The interesting thing is that many stocks had a rough year this year (at least they did until the last few weeks of December), but I did not find that many compelling opportunities. When valuing a stock, I often found that even though the stock sold off, it was not cheap because the higher discount rate I used to match the rise in risk free rates.

At this point, I would like to reiterate what my ideal stock selection criteria is. The goal is to find out of favor companies that are trading below their intrinsic value. This happens due to a market-wide panic, certain sectors are in a slump, individual companies not meeting Wall Streets expectations, or sometimes a temporary scandal. Depending on the company, its intrinsic value is best determined by appraising the value of its tangible assets, or valuing the company on its earnings power. Most companies are overvalued, so the challenge is to keep turning over rocks and being patient for the right stock trading at a discount.

Portfolio Composition

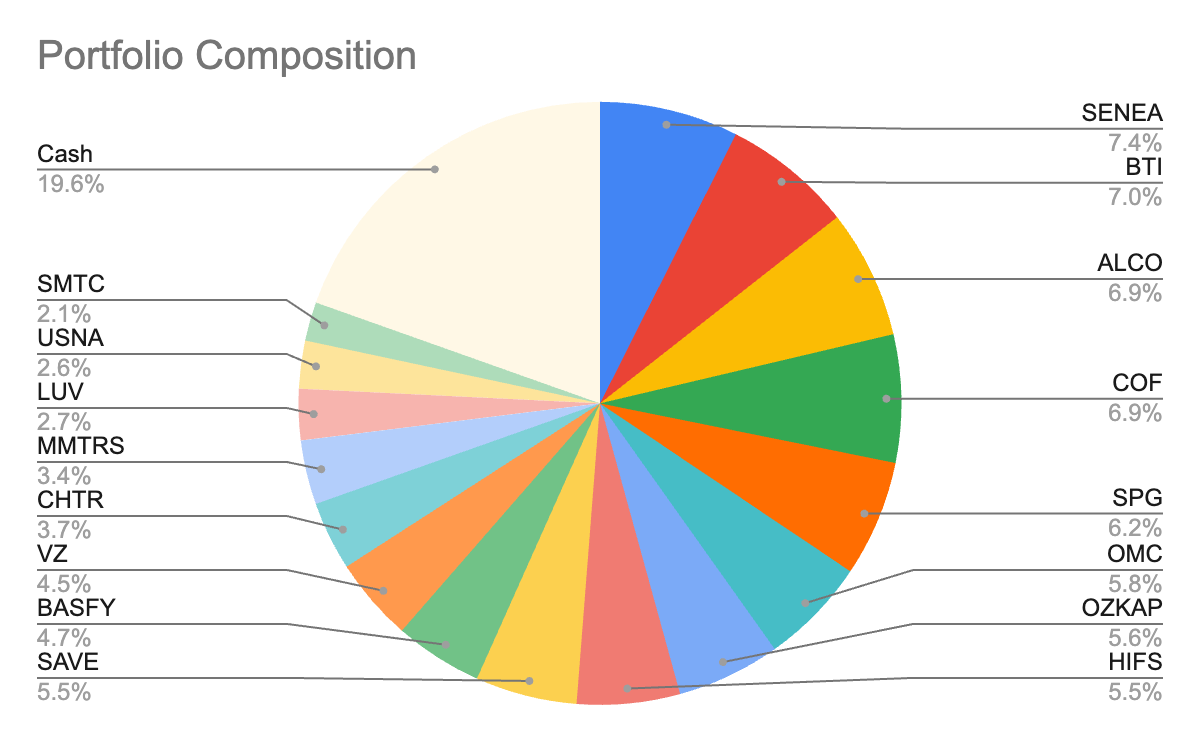

The current allocation of the portfolio is shown in the chart below. Currently, the portfolio consists of 16 stocks. The top five largest positions are Seneca Foods, British American Tobacco, Alico, Capital One, and Simon Property Group.

Current Holdings

My portfolio generally consists of two types of stocks. The first is quality companies that I believe are facing a negative setback in which the market has over-reacted to. I will typically perform more due diligence on these companies, and size the position around 10% of the portfolio at purchase.

The other stocks I hold could be trading at a low valuation multiple, be a net-net, special situation, etc. I usually do less due diligence on these companies, and hold them for shorter periods of time. Accordingly, I take a basket approach where each individual stock makes up 2-5% of the portfolio.

British American Tobacco is my largest position by cost, and performed quite mediocre for the year. The company faced many headwinds such as the menthol flavor ban in California, the looming national menthol ban, customers trading down to cheaper brands due to the economy, and cigarette volume declines that were greater than the historical 5% yearly decline. To top it off, late in the year the company announced an impairment of its intangible assets relating to its American cigarette brands.

The good news is that BTI was was able to compensate its weak performance in the US by having decent results in some of its international markets. Despite the weakened volumes, profits still increased overall for the year. Additionally, the management stated that its non-combustible tobacco products should become profitable next year. This could change sentiment for the stock if it does come into fruition. Lastly, the unrealized losses are somewhat dampened by BTIs strong dividend yield.

The business performance of Alico was pretty bad this year due to the impact of hurricane Ian in 2022. The poor orange crop yields were the reason why the stock was out of favor this year, and part of the reason why I was interested in the company. The management is optimistic that next year will produce better results. The big news for Alico was that they announced that they have sold off their remaining ranch land in a deal that will close early in 2024. Alico has been gradually selling off its ranch land for the past several years, and I anticipated it would take a few more years to complete the sales. The company said it would use part of the proceeds to pay down debt, and I hope they use the rest to of the cash to do a special dividend or large share buyback.

Back in the stock market panic of March 2020, I bought three stocks that formed the beginning of the current iteration of my stock picking portfolio. Those stocks were Emerson Electric, Capital One, and Simon Property Group. The goal was to buy these depressed, high quality companies and hold them for at least five years. To this day, I still hold Capital One and Simon, but earlier this year I sold Emerson Electric. While EMR had solid business performance, I was becoming nervous of their capital allocation decisions, so unfortunately the company did not last five years in my portfolio.

Recently I purchased some Spirit Airlines as a merger arbitrage, since Jet Blue is attempting to acquire the company. If the deal goes through at the original acquisition price, my holding will produce around a 100% gain. The reason there is a large gap between the current stock price and the acquisition price is because the market is not feeling certain the deal will go through due to regulatory concerns. Last month Jet Blue/Spirit went to court with the DOJ to determine the fate of the merger. The verdict is supposed to be released in January 2024, but the reports of the court proceeding suggest that Jet Blue/Spirit made some solid arguments.

A good example of higher interest rates affecting financial assets is the Bank OZK preferred stock that I purchased at $15 a share. The preferred stock has a par value of $25, and when issued it had a dividend yield of 4.6%. However, the yield based on my purchase price was around 8%. The reason the price of the preferred stock is down so much is due to increase in interest rates making the original yield of the preferred not very attractive compared to the risk free rate. Then add on the banking crisis fears causing bank stocks to decline. As rates go down, the yield on OZKAP will look more attractive to investors, and it is likely to revert closer to the $25 par value. This should provide a nice capital gain, plus continued high dividend yield.

Finally, I want to discuss Hingham Institute for Savings, a small Boston area bank. Hingham’s sole focus is making loans to multifamily real estate investors. This bank has been known to have high quality management, industry low expense ratios, and historically has had low loan losses. Since the bank is known for its quality, it usually trades above 1.5x book value, and often over 2x book value. However, HIFS has seen their earnings decrease due to high deposit costs, which have beat up the stock price. I was able to buy shares of Hingham for 1x book value. If interest rates stop increasing or decline, Hingham’s deposit costs should get back under control and the stock should rally back to its normal valuation.

Stocks Purchased in Q4

Stocks Sold in Q4

Dividends

The following are the dividends received in Q4.

For the full year the portfolio generated $2,823.33 in dividends.